Kimbal Establishes Australia & New Zealand Headquarters in Victoria, Strengthening Australia-India Collaboration in Smart Energy

Published on 21 July 2026

With 495 GW of installed capacity and an energy shortfall of just 0.1%, India, a nation of 1.4 billion people, has achieved what few developing economies have: near-total balance between power supply and demand.

Not long ago, flicking a light switch in India carried an air of uncertainty. Across the country, households planned their routines around power cuts, students studied by candlelight, and neighbourhoods slipped into darkness with unsettling regularity. Small and medium-sized enterprises, ranging from metal workshops and textile units to corner stores and family-run shops, depended on diesel generators to keep their businesses running. In rural areas, farmers timed irrigation to the few predictable hours of supply, while cities adapted to the rhythm of load-shedding. Electricity was not a guarantee but a daily negotiation between ambition and infrastructure. A growing economy found itself constrained by the limits of an overstretched grid, its progress dimmed quite literally by the shortage of reliable power.

India has also nearly doubled its installed capacity from 249GW in 2014 to over 495GW as of August 2025, according to data from CEA reports. India’s synchronized National Grid, now interconnected with Bangladesh, Bhutan, Myanmar, and Nepal, has positioned the country as a net exporter of electricity and a stabilizing force in South Asia’s power market.

Before India’s recent surge in performance, the country’s power sector lagged, constrained by supply side inefficiencies and structural limitations. By the 2010s, two decades of economic liberalisation had reshaped consumption patterns: a growing middle class was buying more appliances, industries were modernising, and urbanisation was accelerating. Demand for electricity soared, but generation, transmission and distribution lagged, creating bottlenecks that were holding the economy back.

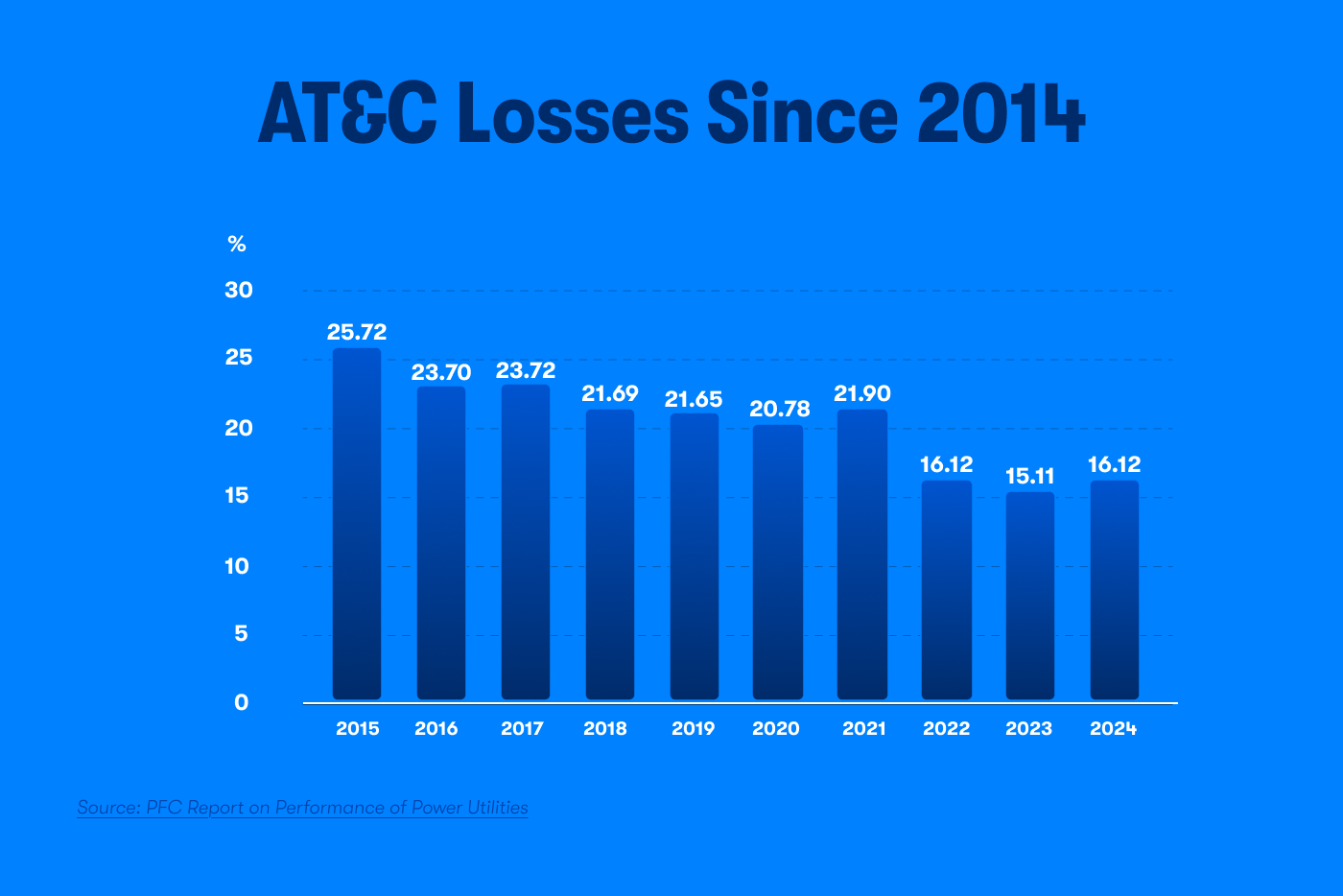

In FY2012-13, India faced peak power deficit of over 12,000 MW, with the northern region alone recording peak power deficits exceeding 8%. According to a study by the Indian Smart Grid Forum (ISGF), India’s Aggregate Technical and Commercial (AT&C) losses exceeded 26% and Transmission and Distribution (T&D) remained above 22%, severely eroding efficiency and causing significant financial loss.

Distribution companies (DISCOMs), many state-owned, were drowning with losses that ran into lakhs of crores of rupees, undermining reinvestment and grid maintenance.

By 2014, India’s installed generation capacity stood at approximately 249 GW, still insufficient to keep pace with rapidly growing requirements.

Though India possessed vast coal reserves, logistical bottlenecks and policy delays meant that domestic coal output was under-utilised forcing costly imports and interrupting fuel security. Hydro output fluctuated dramatically with monsoon variability, and renewable generation was still a marginal contributor.

India’s power sector today reflects a decade of structural transformation. The country has evolved from crisis management to system optimisation, building one of the most dynamic and diverse energy ecosystems in the developing world.

A Decade of Capacity Expansion

Over the last ten years, India has nearly doubled its total installed capacity from 239 GW in 2014 to 495 GW as of August 2025. According to the Press Information Bureau (PIB), India has achieved 235 GW from non-fossil fuel sources, comprising 226 GW of renewable energy and nearly 9 GW of nuclear power. Together, these account for about 49% of total installed capacity, bringing the nation closer to its COP26 target of 500 GW of non-fossil capacity by 2030.

Solar energy has led the charge, growing from less than 3 GW in 2014 to over 110 GW today, placing India among the top three solar producers globally. Wind energy has also crossed 51 GW, while hydroelectric capacity stands near 48 GW, reflecting a diversification unseen a decade ago.

Diversifying the Energy Mix

According to The Times of India, non-renewable energy, particularly thermal plants dominated the system in 2013, accounting for nearly 80% of total generation.

By 2025, that share has fallen to around 50%, even as total generation has grown substantially. This shift was made possible through massive renewable deployment, coal-efficiency upgrades, and investments in flexible generations.

The result is a grid that is not only larger but also more balanced, capable of absorbing variable renewable output while maintaining reliability. India’s non-fossil generation capacity now is nearly equivalent to the entire installed power capacity the nation had in 2013.

A Stronger, Smarter Grid

India’s transition from fragmented regional grids to a fully synchronised National Grid has been pivotal.

Inter-regional transfer capacity has expanded to nearly 120 GW, ensuring that surplus power from one region can seamlessly meet deficits in another.

The grid is now synchronously connected with Bangladesh, Bhutan, Myanmar, and Nepal, enabling cross-border power trade and establishing India as a net electricity exporter.

Digitalisation has also transformed system operations:

Universal Access and Rising Consumption

Beyond generation, India’s most remarkable progress has been in access and reliability. Under the Saubhagya Yojana, more than 2.86 crore households were connected to the grid, achieving universal village electrification and near-complete access to power across the country. As per the Ministry of Power, in 2014, the average daily power availability in rural areas stood at barely 12.5 hours; today, it exceeds 21 hours, while urban centres enjoy over 23 hours of uninterrupted supply, a testament to how far India’s electricity network has evolved in just a decade.

At the consumer level, per-capita electricity availability increased from 950 kWh in 2013 to nearly 1,400 kWh in 2025, reflecting both greater access and reliability. Meanwhile, smart-meter penetration is expanding rapidly under schemes such as the Revamped Distribution Sector Programme (RDSS). Financially, collection efficiency and AT&C loss reduction are improving, supported by digitalisation and the Late Payment Surcharge (LPS) mechanism.

Financial and Efficiency Reforms

India’s progress isn’t limited to hardware; it’s also about institutional reform.

Through programmes like UDAY (2015) and the Revamped Distribution Sector Scheme (RDSS, 2021), the country has addressed chronic inefficiencies in state-run distribution companies (DISCOMs).

Key achievements include:

These financial and operational improvements have strengthened the entire electricity value chain from generator to consumer.

AT&C Losses Since 2014 (Source: PFC Report)

While India’s power sector has made extraordinary progress, surplus generation capacity does not automatically translate into a frictionless system. Beneath the macro-level success story lies persistent operational, financial, and structural challenges that continue to test the system’s resilience.

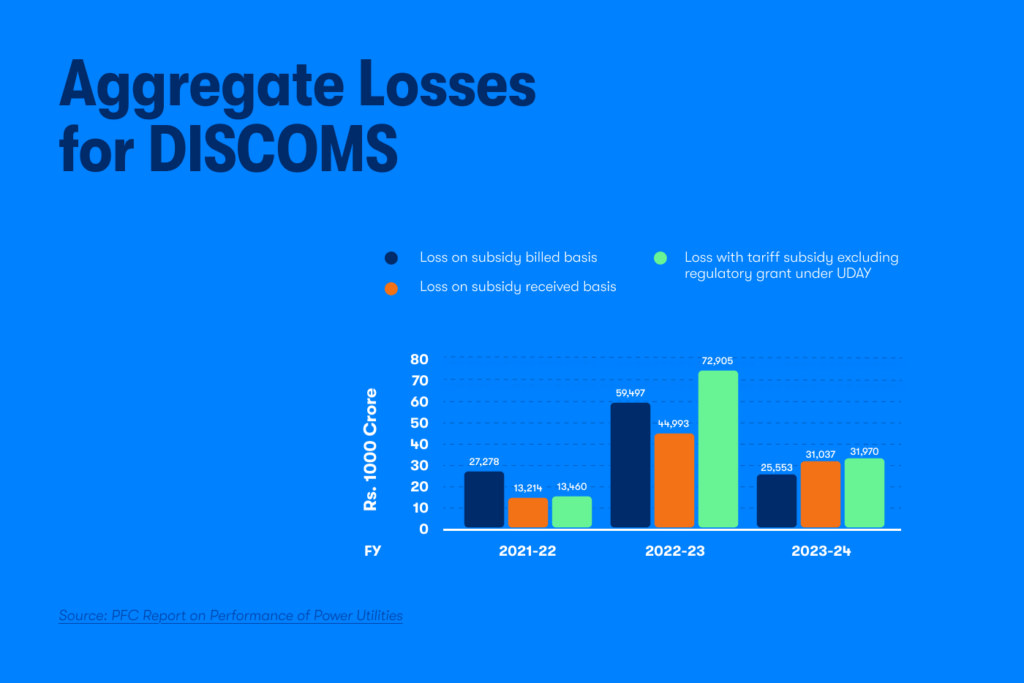

First, distribution remains the weakest link in the electricity value chain. Despite financial restructuring through programmes like Ujwal DISCOM Assurance Yojana (UDAY) and Revamped Distribution Sector Programme (RDSS), several state-owned DISCOMs continue to face high losses and liquidity constraints.

Aggregate Losses for DISCOMS (Source: PFC Report)

According to the Power Finance Corporation’s (PFC) report on Performance of Power Utilities (2023-24), even though aggregate losses decreased, accumulated losses still exceed Rs7 Lakh crore, with AT&C losses averaging over 16% nationally and exceeding 25% in some states. Inefficient billing, delays in subsidy disbursals, and politically driven tariff controls remain persistent issues.

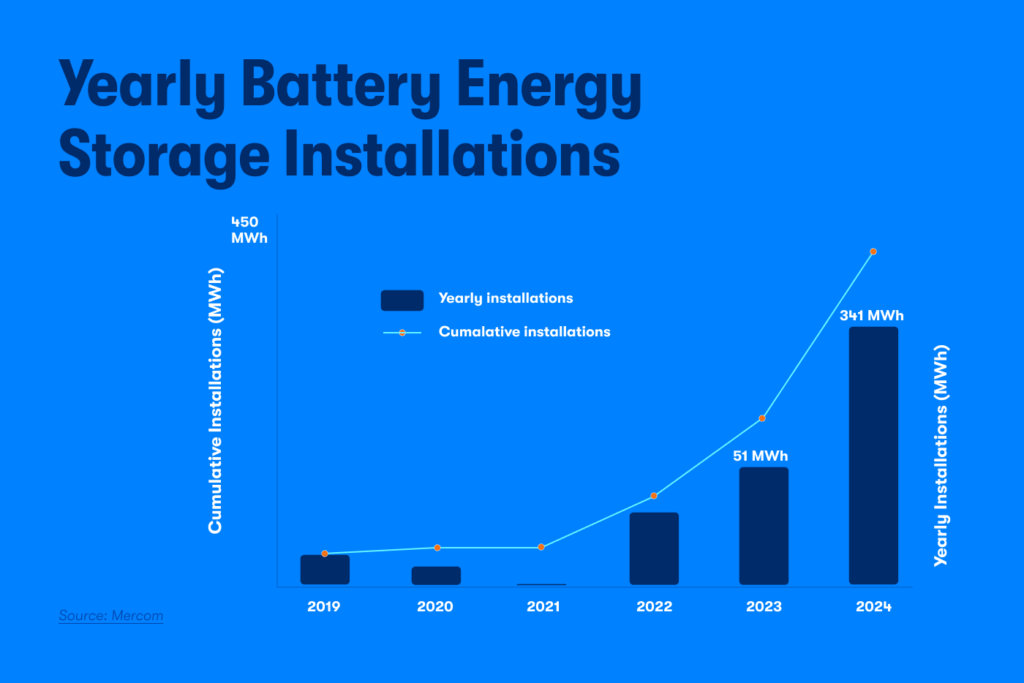

Second, renewable integration poses new challenges. With renewables now contributing almost 50% of installed capacity, the grid faces increasing variability and intermittency. The need for flexible generation, energy storage, and grid balancing is greater than ever. The Central Electricity Authority (CEA) estimates that India will require over 70 GW of battery storage capacity by FY2031-32 to stabilise renewable fluctuations, yet installed storage remains below 1 GW today, as per The Economic Times.

Finally, though we have seen a significant reduction in coal dependence, it remains significant. Thermal power still accounts for more than half of India’s electricity generation, and fluctuations in coal supply chains, import prices, and monsoon-linked demand continue to test grid stability. Transitioning from this base-load reliance to a more flexible, low-carbon system remains a central policy challenge.

A nation where 1.4 billion lives depend on reliable people, India has achieved what once was believed to be improbable, creating a balance between supply and demand in the most populous nation in the world.

Next steps involve focusing on achieving distribution efficiency, increasing storage capacity, and accelerating decarbonisation efforts to meet global commitments.

In this next phase, smart technologies will define how to effectively manage this surplus power to serve its citizens. A recent LinkedIn poll found that 41% of respondents see “better control over energy use” as the biggest benefit of smart meters, followed by “no billing errors and guesswork” (29%) and “efficiency across systems” (24%). These insights underscore that the next frontier isn’t just more power; it’s smarter power, where consumers play an active role in managing energy demand and sustainability.

See how Kimbal is leading the way in smart technologies for a sustainable future:

Published on 21 July 2026

Published on 13 July 2026

Published on 2 July 2026

Your email address will not be published. Required fields are marked *